By Greg Hammett, Yohannes Kidane, and Matt Sipple

Introduction

Are you tired of losing Interagency Agreements (IAA) through lengthy e-mail communications? If so, then good news! On October 1, 2022, Federal agencies will be required to implement the new Department of Treasury (Treasury)-developed system, G-Invoicing, to execute any new IAAs. The days of coordinating IAAs through numerous e-mails, manual record keeping, and version control challenges of the 7600A: General Terms & Conditions (GT&C)(i) and 7600B: Order Form(ii) are over. G-Invoicing will be leveraged as a workflow and brokage system to facilitate drafting, reviewing, approving, and settling funds for Buy/Sell IAAs. This deadline is quickly approaching wherein many agencies have been preparing for; however, many program, regional, and field offices have not yet received training or thought about their team members’ roles or what approval process may be required to suit their offices’ unique needs.

The deadline is not the only date relevant to G-Invoicing. There is an additional requirement to convert any “In-Flight” agreements with an ending Period of Performance (POP) beyond September 30, 2023, into G-Invoicing by October 1, 2023, regardless of when it was initiated.

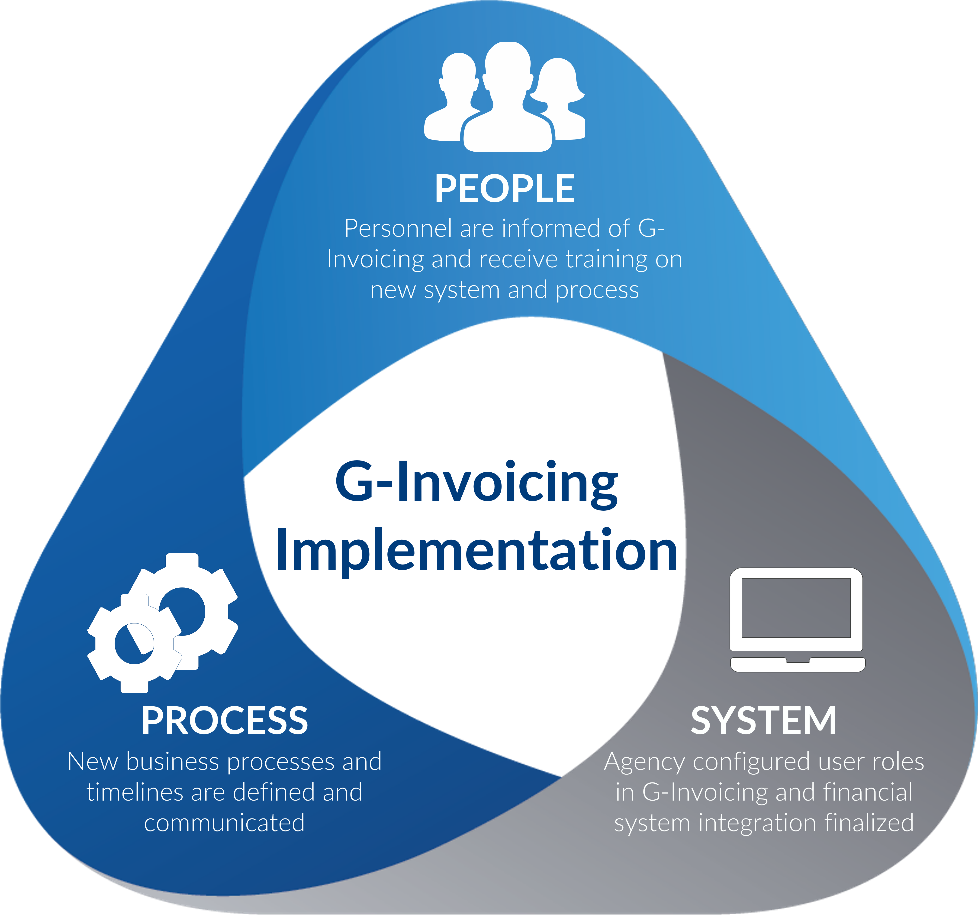

As the first deadline approaches and offices scramble to prepare for the impending October 1 change, each office should focus on three key aspects to prepare for a successful G-Invoicing transition: People, Processes, and Systems.

People

People are the keystone to process change and define the success or failure of change management. You can have the most sophisticated processes and systems in place, but if the people involved are not knowledgeable or do not buy into the criticality of the process or system, success is inevitably impossible.

There are several different organizational levels that are primarily impacted by G-Invoicing: cabinet-level agency administrators, component-level administrators, and office-level personnel and end-users. Typically, the administrators have been involved in the agency-level planning, so the primary focus this close to implementation is making sure the office-level personnel and end-users impacted are clear on how their jobs will change with this new system. The key to preparing your people at all levels for G‐Invoicing is change management and communication to the personnel impacted by the G-Invoicing implementation.

Each Federal agency is required to submit quarterly implementation updates and have a cross-functional team in charge of driving the implementation of G-Invoicing with representation from each component; however, all levels of the organization may not be reached by communication, and it is critical to impart communication to each office’s end-users. Furthermore, offices should consider taking a more proactive stance as the implementation date approaches and reach out to the agency’s implementation team or the component’s representatives to solidify the implementation plan. At each level, organizations should evaluate various considerations, including, but not limited to:

- Have all impacted personnel within the organization been identified and mapped to G-Invoicing roles?

- Have personnel been formally informed of the G-Invoicing transition and the required actions to complete by October 1, 2022?

- Has the agency’s G-Invoicing implementation team determined and communicated how personnel will be trained and provided access to internal and/or the Bureau of Fiscal Service (Fiscal Service)-developed trainings?

- How does the agency confirm that personnel have been trained for the G-Invoicing system and any manual workarounds?

- Has the agency communicated the new processes related to executing IAAs and funds settlement in G-Invoicing, including any manual workarounds or process automation around recording G-Invoicing events within the financial system?

- Are personnel clear on the new processes for G-Invoicing?

- Have each office’s personnel reached out to coordinate with trading partners?

- Who will be responsible for reviewing performance/funds settlement transactions in G-Invoicing?

- Are individuals reviewing performance/funds settlement transactions in G-Invoicing knowledgeable of the IAA and can they confirm the accuracy and validity of transactions submitted?

Change management for the impacted personnel is critical, but process considerations also need to be finalized to ensure clear communications can be disseminated on process changes.

Processes

Through the transition to G-invoicing, many internal processes will be adjusted and the agency, as well as individual offices, will need to evaluate how their processes will move from what is typically a very manual process to a more automated workflow. Below is a list of process change management considerations:

- How will new user or user modification requests be submitted, validated, and approved?

- How will segregation of duties be evaluated and enforced?

- What specific workflow considerations, such as special approvals, will be required based on risks, including dollar threshold, assisted acquisitions, legal concerns, programmatic considerations, etc.?

- Will G-Invoicing interface with the financial system or will manual entries be entered in the financial system for completed actions in G-Invoicing?

- Will there be an interim process(es) and a final process to move from fully manual input to fully automated system interfaces between G-Invoicing and the financial system?

- If G-Invoicing will not interface with the financial system, what reconciliations need to be implemented to confirm the completeness and accuracy of orders in the financial system versus G-Invoicing?

- Will the “Work Basket” panel located in G-Invoicing be sufficient to manage and prioritize agreements based on the volume of transactions or will a manual process be needed to track and prioritize IAAs in the workflow?

- Will open agreements completed pre-G-Invoicing be converted into G-Invoicing?

- How will the offices handle IAAs with trading partners that did not convert to G-Invoicing?

- How will the offices make sure information required for the financial system that is not required by G-Invoicing will be included and communicated in the IAA?

- How will agencies confirm G-Invoicing performance transactions by Order match the payments and collections recorded in the financial system by Order and what will happen if it does not match?

Many of the people and process considerations will, ultimately, result in system impact considerations that need to be evaluated and implemented ahead of the October 1, 2022, deadline.

Systems

Systems

There are two systems that each agency needs to focus on: G-Invoicing and the financial system. However, depending on how your agency implements the IAA process, there may be other, additional systems that need to be considered. Based on decisions made at the people- and process-levels, specific system configuration considerations need to be made in G-Invoicing regarding user roles, workflows, and organizational structure. Additionally, the financial system needs to be configured for the Application Program Interface (API) and mapping and validation rules, as well as other functionalities. Below are some system considerations:

- How will the G-Invoicing organization structure need to be configured, down to the office-level?

- Will any components or offices require special G-Invoicing organizational configurations?

- How will the initial list of users be identified, uploaded, and mapped to roles in G-Invoicing?

- How will G-Invoicing workflows be configured and what special rules will need to be configured?

- Will the Enterprise Resource Planning (ERP)/Software providers have the G-Invoicing interface for the GT&C and Orders configured by October 1, 2022?

- Will GT&C, Orders, and performance transactions be tested to confirm the automatic processing works, as designed when initiated in G-Invoicing?

- What combination of Agency Location Code (ALC) and Treasury Account Symbol (TAS) components will need to be configured for each office to appropriately limit access and reduce inaccurate use of TASs?

G-Invoicing has the opportunity to greatly increase coordination between trading partners and, by extension, reduce the current challenges with Buy/Sell intragovernmental transactions. So, what is next?

- Evaluate if G-Invoicing impacts your role within your agency

- Coordinate internally to identify your agency’s G-Invoicing cross-functional team or component representatives and request additional information about the implementation plan and internal training plan

- Visit the Treasury Fiscal Service’s G-Invoicing Website(iii) to learn more about G-Invoicing, evaluate impacts to your organization and role, and leverage the developed training resources to see G-Invoicing functionality.

Connect With Us

This publication is for informational purposes only and does not constitute professional advice or services, or an endorsement of any kind. Readers should first consult with a professional before acting regarding the subjects mentioned herein.

Kearney & Company, P.C. (Kearney) is a Certified Public Accounting (CPA) firm that is focused on providing accounting and consulting services to the Government.

(i) Department of Treasury Bureau of Fiscal Service, G-Invoicing, Resources, https://fiscal.treasury.gov/files/forms/fs-form-7600a.pdf

(ii) Department of Treasury Bureau of Fiscal Service, G-Invoicing, Resources, https://fiscal.treasury.gov/files/forms/fs-form-7600b.pdf

(iii) Department of Treasury Bureau of Fiscal Service, G-Invoicing, About G-Invoicing, https://fiscal.treasury.gov/g-invoice/about-g-Invoicing.html